A Primer On Sound Money: Gibson’s Paradox And The Fatal Error Of Keynes And Friedman

by GoldMoney •

Introduction

Thomas Tooke in 1844 is generally thought to be the first to observe that the price level and nominal interest rates were positively correlated. It was Keynes who christened it Gibson’s paradox after Alfred Gibson, a British economist who wrote about the correlation in 1923 in an article for Banker’s Magazine. Keynes called it a paradox in 1930, because there was no satisfactory explanation for it. He wrote that “the price level and the nominal interest rate were positively correlated over long periods of economic history”i. Irving Fisher similarly had difficulties with it: “no problem in economics has been more hotly debated,”ii and even Milton Friedman was defeated: “The Gibson paradox remains an empirical phenomenon without a theoretical explanation”.iii Others also attempted to resolve it, from Knut Wickseliv to Barsky & Summers.v

Monetary theory would suggest the correlation should have been between changes in the level of price inflation and interest rates. This is the basis upon which central banks determine monetary policy, and now that the gold standard no longer exists, it is probably assumed by those that have looked at the paradox that it is no longer relevant. This appears to be a reasonable explanation for today’s lack of interest in the subject, with many professional economists unaware of it.

Those economists who have examined the paradox generally agree that it existed. This paper will not go over their old ground other than to make a few pertinent observations:

· Data over the period covered, other than prices for British Government

Consols cannot be deemed wholly reliable for two reasons. Firstly, price data from 1730 to 1930, the period observed, cannot be rigorous; and secondly any observations of price levels by their nature must be selective and subjective as to their composition.

· Attempts to construct a theory to explain the paradox after the Second

World War differ from earlier attempts, because the more recent academic consensus dismisses Say’s Law, otherwise known as the law of the markets. Barsky & Summers in particular resort to mathematical explanations as part of their paper, thereby treating it as a problem of natural science and not a social science.

· The economists who have tackled the problem were unaware of the

Austrian School’s price and time-preference theories, or have dismissed them in favour of Neo-Keynesian and monetary economics. The silence of the Austrian School on the subject is an apparent anomaly.

The Author shows that the theoretical reasoning of the Austrian School leads to a satisfactory resolution of the paradox without having recourse to questionable statistics or mathematical method.

The paradox

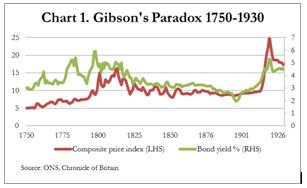

Gibson’s paradox is based on the long-run empirical evidence between 1730 and 1930, a period of 200 years, when it was observed by Arthur Gibson that changes in the level of the yield on British Government Consols 2 ½% Stock positively correlated with the wholesale price level. No satisfactory theoretical explanation for this correlation has yet been published. It is shown in Chart 1 (Note: annual price data estimates from the Office for National Statistics are only available from 1750).

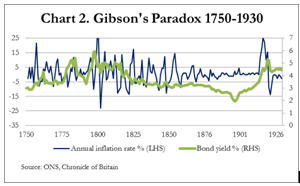

The quantity theory of money suggests that instead there should be a strong correlation between changes in interest rates and the rate of price inflation. However there is no discernible correlation between the two. Contrast Chart 2 below with Chart 1 above.

If Gibson’s paradox is still relevant it presents a potential challenge to monetary policy. The question arises as to whether it is solely an empirical phenomenon of metallic, or sound money, or whether its validity persists to this day, hidden from us by the expansion of fiat currency and bank credit, and the central banks’ success in substituting pure fiat currency in place of sound money. If the paradox is solely a consequence of metallic, or sound money, it might pose no threat to the modern currency system; otherwise it may have profound implications.

Modern macroeconomists appear ill-equipped to tackle this issue. The paradox is essentially a market phenomenon and macroeconomics is at odds with markets. An economist who favours macroeconomic theory will acknowledge a primary function of the state is to intervene in markets for a better outcome than a policy of laissez-faire; and that the needs and wants, the purposeful actions of ordinary people, collectively through markets free of exogenous factors, can be improved by government intervention. Yet it is ordinary people and their businesses that were behind the relationship between the interest rate on gold or gold substitutes and wholesale prices during the period the paradox was observed. For this reason an approach to the problem that is consistent with Say’s law and denies the validity of conventional neo-classical economic theory is more likely to resolve the paradox.

Why Say’s law is important

Say’s law describes the fundamental framework within which markets work. By implication it holds that each one of us produces a good or service so that we can buy the goods and services we want: we produce to consume so we are both producers and consumers. Put another way, we cannot acquire the wide range of things we need or want without providing our labour and specialist skills for profit, the profit we require to sustain ourselves. Furthermore, we may choose to defer some of this consumption for future use when it is surplus to our immediate needs. Deferred consumption is saving, the accumulation of wealth, which is either redeployed by the individual to maximise his own productive capacity, or made available to other individuals to enhance their skills for a return. The medium that facilitates all these activities is money, which effectively represents stored labour. It stands to reason that the money used has to be acceptable to all parties.

The primary purpose of money as a transaction medium is to enable all goods and services to be priced, thereby removing the inefficiencies of bartering. Money enables a buyer to compare the cost and benefits of one item against another, and for producers to compete and provide what consumers most want. The forum for this competition is the market, a term for an intangible entity, which facilitates the exchange of goods and services between producers and consumers. Consumers decide how they wish to allocate the fruits of their labour, and it is up to producers to anticipate and respond to these decisions. If someone is not productive and has no savings in order to consume and survive, he or she will require a subsidy, such as welfare or charity, provided from the surplus of other producers. Despite the flexibility money provides these human actions, they cannot be separated.

Therefore everyone is both a producer and consumer, or if unemployed, indirectly so. And it is the individual decision of the consumer what proportion of his production profit to put aside, or save for the future. Say’s law describes economic reality, and was generally recognised as the fundamental law of economics until about 1930. But it was an inconvenient truth for some thinkers in the late nineteenth century, most notably for Karl Marx, who advocated state ownership of the means of production, and the national socialists of the early twentieth century who advocated state control of production through regulation. Both socialism and fascism were attempts by the state to subvert the free market process that allowed producers to have the freedom to respond to consumer demands, so both creeds contravened Say’s law. Finally, Keynes began in the 1930s to work up a proposition to separate production from consumption and to dismantle the relationship between current and deferred consumption, which culminated in his General Theory, published in 1936.vi

Keynes’s influence on modern economics is fundamental to today’s macroeconomic theories and has led to a widespread academic denial of Say’s law. Modern academics, including Keynes himself, were therefore unsympathetic with the theoretical framework required to address the paradox, if only on the basis that it was commonly accepted over the period being considered. It is also an anomaly that the subject seems to have escaped the attention of London- based economists of the Austrian School, such as Robbins and Hayek for whom Say’s law remained a fundamental basis of economic theory.

The financial and economic background to 1730-1930

Gibson’s paradox was recorded in Britain, so we must first examine the social and economic conditions that pertained in order to understand the circumstances behind the paradox, and to eliminate the possibility it was the result of circumstances rather than evidence of sound theory yet to be explained.

The increase in the above-ground stock of gold, which was the foundation of money and all money substitutes for much of the time, was a potential factor over the period observed. Uses for gold included jewellery and other adornments as well as money mostly in the form of coin, so it is not possible to establish accurately the money quantity. The observation was of British prices and bond yields, so it is the quantity of gold in circulation as money in Britain which matters, though there is the secondary consideration of gold in circulation in the hands of Britain’s trading partners. During the whole period with the exception of the disruption caused by the Napoleonic wars, the quantity of gold was regulated between Britain and her trading partners solely by the demands of trade. Given the low level of peacetime intervention by governments in free markets at that time, differences in prices between countries were arbitraged through gold movements. We can therefore reasonably take the global quantity of aboveground gold stocks as indicative of the quantity of money in circulation regulated only by the market’s requirements; though bank credit or the over- issue of unbacked money became an increasing cyclical factor following the Bank Charter Act of 1844.

Prior to the Napoleonic Wars, Britain began to build herself into the most powerful trading economy in history, aided by her overseas possessions and influence, together with the declining influence of Spain after the War of the Spanish Succession. The development of trade with India in the eighteenth century will have increased British demand for gold. The wars against France following the French Revolution were costly both socially, involving nearly half a million men in the army and navy, and financially leading to a drain on gold reserves. Prices rose, driven by the increase in unbacked money substitutes

issued by the country banks, and by the diversion of financial resources to support the war effort. This led to the suspension of specie payments on demand against bank notes in 1797. By that time the public had become used to accepting bank notes as a valid substitute for gold, so it continued to accept them in lieu of specie.

Following the Napoleonic wars, the economy had to adjust to peacetime. The Bullion Committee, which had been formed in 1810, recommended a resumption of specie payments to address the problem of rising prices, a recommendation rejected by the government. It was not until 1819, when the war had been over for four years that a second committee under the chairmanship of Robert Peel again recommended a return to specie payments, and from 1821 onwards a gradual resumption of cash payments for banknotes resumed.

The over-issue of notes by the banks during the Napoleonic wars led to the failure of eighty country banks in 1825. This was followed by two Acts of Parliament: in 1826 restricting the Bank of England’s monopoly to a radius sixty- five miles from London but permitting it to compete with branches in the provincial towns; and in 1833 withdrawing the Bank of England’s monopoly altogether. Banks were then free as a consequence to expand from single-office operations into branch networks through a process of expansion and mergers. The foundation of today’s British banks dates from this time.

During this period the debate about the future of money and banking intensified, with the banking school arguing that banks should be free to issue notes as they saw fit, so long as they were prepared to meet all demands for encashment into specie. The currency school argued instead for bank note issues to be tied strictly to specie held in reserves. The controversy between these two schools ended with the Bank Charter Act of 1844, which required the Bank of England to back its note issue with gold, with the exception of £14,000,000 of unbacked notes already in circulation. The intention was for Bank of England notes to gradually replace those issued by other banks in England and Wales (Scottish banks still issue their own notes to this day).

Thus it was that the Bank Charter Act of 1844 sided with the currency school, so far as the note issue was concerned; but by neglecting the issuance of credit, modern fractional reserve banking was born.

It can be seen that Gibson’s paradox had to survive substantial variations of economic and monetary conditions likely to disrupt any correlation between the level of wholesale prices and interest rates. If there was a common factor over the two centuries, it was that the domestic UK economy expanded rapidly, facilitated initially by a developing network of canals, which in addition to river and sea navigation enabled the transport of goods throughout the country for the first time. As the industrial revolution progressed, the new science of thermodynamics led to the development of steam power, fuelled by coal which was found and mined in abundance. The mechanisation of factories and mills together with the subsequent development of railways rapidly increased both productivity and the speed of transport and communications. Her position as an

important global power gave Britain access to raw materials and overseas markets to fuel economic and technological progress. Britain was so successful that before the First World War eighty per cent of all shipping afloat at that time had been built in Britain. Finally, in the post-war decade to 1930 Britain underwent massive social and political changes, which were generally destructive to the accumulated wealth of the previous century.

Gold supply

Without an increase in the quantities of gold available the expansion of economic activity brought about by the industrial revolution would have been expected to lead to a trend of falling prices. As it was, new mines were discovered, notably in California, the Klondike, South and West Africa, and Australia. By 1730 the estimated aboveground stocks accumulated through history were about 2,400 tonnes, and by 1930 they had increased to 33,000 tonnes.vii Britain’s population increased from roughly seven million to forty-five million. In other words, the quantity of gold available for money increased at roughly double the rate of the British population over the two centuries.

Other things being equal, the net monetary effect from the increase in the quantity of above-ground gold stocks can be expected to reduce its purchasing power relative to goods; but it is an historical fact that the rapid industrialisation over the period raised the standard of living and life expectancy for the average person considerably, thereby offsetting the inflationary price effects of increased above-ground stocks, so much so that prices appear to have fallen by 20% between 1820 and 1900 according to the ONS figures used in Chart 1.

The quantity theory of money

The quantity theory as it is generally understood today dates back to David Ricardo, who ignored the transient effects of changes in the quantity of money on prices in favour of a long-run equilibrium outcome. In 1809 Ricardo took the position that the reason for the increase in prices at that time was due to the Bank of England’s over-issue of notes. His interest in this respect glossed over the short-run distortions identified by Cantillon and Hume. In the Ricardian version an increase in the quantity of money would simply result in a corresponding rise in prices.

While this relationship is intuitive, it makes the mistake of dividing money from commodities and putting it into a separate category. An alternative view, consistent with the theories of the Austrian School, is to regard money as a commodity whose special purpose is to act as a fungible medium of exchange, retaining value between exchanges. This being the case, it must be questioned whether or not it is right to put money on one side of an equation and the price level on the other.

This is not to deny that a change in the quantity of money for a given quantity of goods affects prices. That it is likely to do so is consistent with the relationship

between the relative quantities of any exchangeable commodities. Furthermore, there is an issue of preferences changing between the relative ownership of one commodity compared with another; in this case between an indexed basket of goods and money. Changes in the general level of cash liquidity can have a disproportionate effect on prices, irrespective of changes in the quantity of money in issue at the time.

By ignoring these considerations it is possible to conclude that changes in the quantity of money in circulation are sufficient to control the price level. It is this assumption that Gibson’s paradox challenges. To modern macroeconomists the price of money is its rate of interest, though to followers of the Austrian school, this is a gross error. To them, the price of money is not the rate of interest, but the reciprocal of the price of a good bought or sold with it. Furthermore, under this logic money has several prices for each good or service, which will differ between different buyers and sellers depending on all the circumstances specific to a transaction. This is consistent with the Austrian school’s observation that prices are entirely subjective and they cannot be determined by formula.

Macroeconomics does not recognise this approach, and averages prices to arrive at an indexed price level. Austrian school economists argue that mathematical methods are wholly inappropriate applied to the real world. Apples cannot be averaged with gin, nor can gin be averaged even with another brand of gin. Averaging the money-values of different products cannot escape this reality.

The rate of interest on money is its time-preference; and again, depending on what the money is intended to be exchanged for its time-preference must match inversely that of the individual good. In other words, by deferring the delivery of a good and paying for it up-front it should be possible to acquire it at a discount. There is the possession of the money foregone, the uncertainty of the contract being fulfilled and the scarcity of the good, which all combine into a time- preference for a particular deferred transaction.

The quantity theory of money ignores this temporal element in the exchange of money for goods. In doing so, it fails to account for the fact that in free markets demand for money, reflected in its time-preference, must correlate with demand for goods. The quantity theory, by putting money on one side of an equation and goods on another suggests the relationship is otherwise.

This gives us an insight into why the quantity theory of money is flawed, and when we explore the Gibsonian relationship between interest rates and the price level it will become obvious why interest rates do not correlate with the rate of price inflation.

The solution to Gibson’s paradox

In the discussion covering the flaws in the quantity theory of money in the previous section clues were given as to how the paradox might be resolved. The starting point is to recognise that money is simply a commodity, albeit with a special function, to act as the temporary store of labour between production and consumption.

We can see that including money, commodities necessary for human progress were in demand during a period of unprecedented economic expansion over the two centuries between 1730 and 1930. In some cases, such as in exchange for harvested grains, the price of gold would have varied from season to season, often wildly. But with all the individual goods, there will have been a match with their time-preferences between manufactured goods and gold and gold substitutes. Therefore, the interest rate on money offered by banks is the other side of the time-preferences of the goods produced by their borrowers, who were predominantly manufacturers and merchants seeking trade finance.

The reason interest rates are set by the demands for money by manufacturers is they have to expend capital in order to produce. Capital becomes one of two essential elements of the price of a future good, the other essential being profit. The capital value of an asset used in production is the sum of the value of output it generates discounted to its present value. If prices of goods are rising, the producer can increase his time-preference in the expectation of higher end- prices for his production. Alternatively, if prices are not rising, or even falling he is limited in his time-preference.

This explains why when prices generally rose, bond yields, as proxy for term interest rates paid by borrowers, also rose. Equally, when prices fell, a producer was less able to bid up his time preferences, so term interest rates fell. In other words, before central banks took upon themselves to control interest rates, interest rates simply correlated to demand for capital from producers.

This analysis of the relationship between prices is wholly in accordance with Carl Menger’s insight, that a price only exists for commodities and goods for which supply is limited to less than potential demand.viii

Post-1930

Post-1930

After 1930 the paradox was still observed until the 1970s, when the relationship appeared to break down.

In the 1970s price inflation according to the ONS accelerated from 5.4% in 1969, to 17.1% in 1974. During that time the Bank of England only increased interest rates under pressure from the markets. Interest rate policy fed a growing preference for hoarding goods and reducing personal cash balances. In this case, the correlation between bond yields and the price level reflected a shift in public confidence in the future purchasing power of the currency, which drove the time-preferences in the market, instead of widespread demand for capital investment.

Bond yields topped out in autumn 1974 before declining; but interest rates finally peaked in 1979/80. This is not fully reflected in the bond yield shown in Chart 4, because the yield curve was sharply negative at that time.

Since that tumultuous decade correlation ceased, and the Bank of England appears to have gained control over interest rates from markets.

It is hardly surprising that when central banks implement monetary policies to ensure that the price level never falls, the normal relationship between the price level and interest rates is interrupted. The relationship between savers and investing producers, which is the basis of the Gibson observation, becomes impaired.

Conclusion

The following question was raised earlier in this paper:

If Gibson’s paradox is still relevant it presents a potential challenge to monetary policy. The question arises as to whether it is solely an empirical phenomenon of metallic, or sound money, or whether its validity persists to this day, hidden from us by the expansion of fiat currency and bank credit, and the central banks’ success in substituting pure fiat currency in place of sound money. If the Paradox is solely a consequence of metallic or sound money it might pose no threat to the modern currency system; otherwise it may have profound implications.

It is clear that the difference between markets historically and those of today is that interest rates were set by the demand for savings to invest in production, while today they are set by monetary policy. Monetary policy is not consistent with the basic function of interest rates, which is to reflect a market rate between savers and borrowers to balance supply and demand. Instead, monetarists believe otherwise, that interest rates can be used to regulate the quantity of money.

Gibson’s paradox is not dependent on metallic or sound money so much as it is dependent on free markets distributing savings in accordance with demand from borrowers investing in their businesses. We must therefore conclude that monetary policies intended to suppress this effect do have profound implications.

Keynes in his General Theory in 1936 wrote the following in his concluding notes:

“I see, therefore, the rentier aspect of capitalism as a transitional phase which will disappear when it has done its work. And with the disappearance of its rentier aspect much else in it besides will suffer a sea-change. It will be, moreover, a great advantage of the order of events I am advocating, that the euthanasia of the rentier, of the functionless investor, will be nothing sudden, merely a gradual but prolonged continuance of what we have seen recently in Great Britain, and will need no revolution.”ix

The long, slow euthanasia of Keynes’s rentier class is what has changed. Businesses obtain the funds for investment from other sources directed by the financial system. Savers are channelled increasingly into stock markets, where they participate in businesses as co-owners, instead of lending to them indirectly through the banking system. The banks provide working capital, mainly through the expansion of bank credit, at rates primarily determined not by supply and demand for savings, but set by central banks.

Central banks’ insistence on monetary solutions to economic problems have not only buried the Say’s law relationship between savers and investing entrepreneurs, they have turned the principal objective of entrepreneurs from patient wealth creation through the accumulation of profits into ephemeral wealth creation through the accumulation of debt. They have been caught up in a credit cycle created by central banks and are no longer borrowing genuine savings from savers who expect to be repaid. If Gibson’s paradox had been satisfactorily explained by Tooke or Gibson, the assumptions behind the quantity theory of money and its derivatives would have been thrown into doubt before they became central to monetary policy.

This is a dramatic claim perhaps, but it might have demolished the suppositions behind the quantity theory of money, which became Fisher’s equation of exchange, and the brand of monetarism followed by the Chicago school under Milton Friedman. Misleading ideas, such as velocity of circulation in the equation of exchange would have not been taken as meaningful economic indicators. As it is Gibson’s paradox is unknown to the majority of economists today, who assume the quantity theory of money is unchallengeable.

So, to put the explanation of Gibson’s paradox at its simplest,

If the prices of goods are expected to rise, then their time preferences are bound to increase, and if they are expected to fall, their time preferences are bound to fall. That is why interest rates correlate with the price level.

Alasdair Macleod

August, 2015.

Source: Goldmoney.com

i J M Keynes, A Treatise on Money, Vol.2 p.1981930

ii Irving Fisher, The Theory of Interest, 1930.

iii Friedman and Schwartz, From Gibson to Fisher, Explorations in Economic

Rersearch NBER vol. 3,2 (Spring)

iv Knut Wicksel, Interest and Prices, 1936, translated from the German, Geldzins und Guterpreiser, 1898.

v NBER Working Paper Series No. 1680 Gibson’s Paradox and the Gold Standard,

1985.

vi J M Keynes, The General Theory of Employment, Interest and Money, 1936.

vii James Turk, The Aboveground Gold Stock: Its Importance and its Size Sept

stock.pdf (accessed July 2015)

viii Carl Menger: Grundsätze der Volkswirtschaftslehre (Principles of

Economics)1871.

ix JM Keynes: The General Theory of Employment, Interest and Money pp 376 of the 1936 edition.

Source:

No comments:

Post a Comment